F-1: Registration statement for securities of certain foreign private issuers

Published on June 29, 2018

As filed with the Securities and Exchange Commission on June 29, 2018.

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

______________________________________________________

Form F-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

______________________________________________________

ENDAVA LIMITED1

(EXACT NAME OF REGISTRANT AS SPECIFIED IN ITS CHARTER)

Not Applicable

(Translation of Registrant’s Name into English)

England and Wales |

7371 |

Not Applicable |

||

|

(State or other Jurisdiction of

Incorporation or Organization)

|

(Primary Standard Industrial

Classification Code Number)

|

(I.R.S. Employer

Identification Number)

|

||

125 Old Broad Street

London EC2N 1AR

United Kingdom

+44 20 7367 1000

(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices)

______________________________________________________

Endava Inc.

441 Lexington Avenue, Suite 702

New York, NY 10017

(212) 920-7240

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

|

Nicole Brookshire

Darren DeStefano

Richard Segal

Cooley LLP

500 Boylston Street, 14th Floor

Boston, MA 02116

(617) 937-2300

|

Ed Lukins

Ed Dyson

Cooley (UK) LLP

Dashwood

69 Old Broad Street

London EC2M 1QS

United Kingdom

+44 20 7785 9355

|

Alan Denenberg

Reuven Young

Davis Polk & Wardwell LLP

1600 El Camino Real

Menlo Park, CA 94025

(650) 757-2000

|

||

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933.

Emerging growth company ý

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period* for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

* |

The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012. |

______________________________________________________

CALCULATION OF REGISTRATION FEE

|

TITLE OF EACH CLASS OF SECURITIES

TO BE REGISTERED

|

PROPOSED

MAXIMUM

AGGREGATE

OFFERING

PRICE(1)(2)

|

AMOUNT OF

REGISTRATION

FEE(3)

|

||

Class A ordinary shares, nominal value £0.10 per ordinary share(4) |

$75,000,000 |

$9,338 |

||

(1) |

Estimated solely for the purpose of calculating the amount of the registration fee pursuant to Rule 457(o) of the Securities Act of 1933, as amended. |

(2) |

Includes the aggregate offering price of additional Class A ordinary shares represented by American Depositary Shares, or ADSs, which the underwriters have the option to purchase, if any. |

(3) |

Calculated pursuant to Rule 457(o) based on an estimate of the proposed maximum aggregate offering price. |

(4) |

These Class A ordinary shares are represented by ADSs, each of which represents one Class A ordinary share of the registrant. ADSs issuable upon deposit of the Class A ordinary shares registered hereby are being registered pursuant to a separate registration statement on Form F-6 (File No. 333- ). |

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

(1) |

We intend to alter the legal status of our company under English law from a private limited company by re-registering as a public limited company and changing our name from Endava Limited to Endava plc prior to the completion of this offering.

|

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and we are not soliciting offers to buy these securities in any jurisdiction where the offer or sale is not permitted.

PROSPECTUS (Subject to Completion)

Issued , 2018

American Depositary Shares

REPRESENTING CLASS A ORDINARY SHARES

___________________________________

Endava Limited is offering American Depositary Shares, or ADSs. The selling shareholders identified in this prospectus are offering ADSs. We will not receive any proceeds from the ADSs sold by the selling shareholders. Each ADS represents one Class A ordinary share. The ADSs may be evidenced by American Depositary Receipts, or ADRs. This is our initial public offering and no public market currently exists for our ADSs. We anticipate that the initial public offering price will be between $ and $ per ADS.

___________________________________

Following this offering, we will have three classes of ordinary shares, Class A ordinary shares, Class B ordinary shares and Class C ordinary shares. The rights of the holders of Class A ordinary shares, Class B ordinary shares and Class C ordinary shares will be identical, except with respect to voting, conversion and transfer rights. Each Class A ordinary share will be entitled to one vote per share. Each Class B ordinary share will be entitled to ten votes per share and is convertible into one Class A ordinary share, subject to certain restrictions. Each Class C ordinary share will be entitled to one vote per share and is convertible into one Class A ordinary share, subject to certain restrictions. Outstanding Class B ordinary shares will represent approximately % of the voting power of our outstanding share capital immediately following the closing of this offering.

___________________________________

We have applied to list our ADSs on the New York Stock Exchange under the symbol “DAVA.”

We are an “emerging growth company” as defined under the U.S. federal securities laws and, as such, have elected to comply with certain reduced public company reporting requirements for this and future filings. Investing in our ADSs involves risk. See “Risk Factors” beginning on page 18.

___________________________________

PRICE $ AN ADS

___________________________________

Price to Public |

Underwriting Discounts and Commissions(1) |

Proceeds to Endava |

Proceeds to the Selling Shareholders |

||||

Per ADS |

$ |

$ |

$ |

$ |

|||

Total |

$ |

$ |

$ |

$ |

|||

(1) |

See “Underwriters” for a description of the compensation payable to the underwriters.

|

Certain of the selling shareholders have granted the underwriters the right to purchase up to an additional ADSs at the initial offering price less the underwriting discounts and commissions.

Neither the Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these securities, or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the ADSs to purchasers on or about , 2018.

___________________________________

MORGAN STANLEY |

CITIGROUP |

CREDIT SUISSE |

DEUTSCHE BANK SECURITIES |

|||

COWEN |

WILLIAM BLAIR |

|||||

___________________________________

, 2018

TABLE OF CONTENTS

Page |

|

Page |

|

___________________________________

We are responsible for the information contained in this prospectus and any free-writing prospectus we prepare or authorize. We have not, and the underwriters and selling shareholders have not, authorized anyone to provide you with different information, and we, the underwriters and the selling shareholders take no responsibility for any other information others may give you. We are not, and the underwriters and selling shareholders are not, making an offer to sell our ADSs in any jurisdiction where the offer or sale is not permitted. You should not assume that the information contained in this prospectus is accurate as of any date other than the date on the front cover of this prospectus, regardless of the time of delivery of this prospectus or the sale of any ADSs.

For investors outside the United States, neither we nor the underwriters nor the selling shareholders have done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction, other than the United States, where action for that purpose is required. Persons outside the United States who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, this offering and the distribution of this prospectus outside the United States.

Following our corporate reorganization, we are a public limited company incorporated under the laws of England and Wales and a majority of our outstanding securities are owned by non-U.S. residents. Under the rules of the U.S. Securities and Exchange Commission, or SEC, we are currently eligible for treatment as a “foreign private issuer.” As a foreign private issuer, we will not be required to file periodic reports and financial statements with the SEC as frequently or as promptly as domestic registrants whose securities are registered under the Securities Exchange Act of 1934, as amended.

Through and including , 2018 (the 25th day after the date of this prospectus), all dealers that effect transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to the dealers’ obligation to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscriptions.

ABOUT THIS PROSPECTUS

Unless otherwise indicated or the context otherwise requires, all references in this prospectus to the terms “Endava,” the “Company,” “we,” “us,” and “our” refer to Endava Limited and our wholly-owned subsidiaries.

Prior to the completion of this offering, we intend to re-register Endava Limited as a public limited company and to change our name from Endava Limited to Endava plc. See “Corporate Reorganization.”

PRESENTATION OF FINANCIAL INFORMATION

Our fiscal year ends on June 30. This prospectus includes our audited consolidated financial statements as of and for the years ended June 30, 2016 and 2017 and our unaudited condensed consolidated financial statements as of and for the nine months ended March 31, 2017 and 2018, which are prepared in accordance with International Financial Reporting Standards, or IFRS, as issued by the International Accounting Standards Board, or IASB. None of our financial statements were prepared in accordance with generally accepted accounting principles in the United States, or U.S. GAAP.

Our financial information is presented in British Pounds. For the convenience of the reader, in this prospectus, unless otherwise indicated, translations from British Pounds into U.S. dollars were made at the rate of £1.00 to $ , which was the noon buying rate of the Federal Reserve Bank of New York on , 2018. Such U.S. dollar amounts are not necessarily indicative of the amounts of U.S. dollars that could actually have been purchased upon exchange of British Pounds at the dates indicated. All references in this prospectus to “$” mean U.S. dollars and all references to “£” and “GBP” mean British Pounds.

We have made rounding adjustments to some of the figures included in this prospectus. Accordingly, numerical figures shown as totals in some tables may not be an arithmetic aggregation of the figures that preceded them.

1

PROSPECTUS SUMMARY

This summary highlights information contained elsewhere in this prospectus and does not contain all of the information that you should consider in making your investment decision. Before investing in our ADSs, you should carefully read this entire prospectus, including our consolidated financial statements and the related notes and the information set forth under the sections titled “Risk Factors,” “Special Note Regarding Forward-Looking Statements,” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” in each case included elsewhere in this prospectus. Unless the context otherwise requires, we use the terms “Endava,” “company,” “our,” “us,” and “we” in this prospectus to refer to Endava Limited and, where appropriate, our consolidated subsidiaries. Our fiscal year ends on June 30.

ENDAVA LIMITED

Overview

We are a leading next-generation technology services provider and help accelerate disruption by delivering rapid evolution to enterprises. We aid our clients in finding new ways to interact with their customers and users, enabling them to become more engaging, responsive and efficient. Using Distributed Enterprise Agile at scale, we collaborate with our clients, seamlessly integrating with their teams, catalyzing ideation and delivering robust solutions. Our approach to ideation comprises an empathy for user needs, curiosity, creativity and a deep understanding of technologies. From proof of concept, to prototype, to production, we use our engineering expertise to deliver enterprise platforms capable of handling millions of transactions per day. Our people, whom we call Endavans, synthesize creativity, technology and delivery at scale in multi-disciplinary teams, enabling us to support our clients from ideation to production.

Waves of technological change are disrupting the nature of competition in every industry. New technologies have enabled the growth and success of companies that leverage these technologies in every aspect of their businesses, or digital native companies, allowing them to be nimble, innovative, data driven and focused on user experience, often through an Agile development approach. Technology has also increased customer expectations, giving customers the ability to choose not only the products and services that they want, but also where, when and how they want them delivered. Incumbent enterprises must undertake digital transformation of their businesses by leveraging technology in order to meet ever-evolving customer expectations and compete with digital native disruptors.

Technological transformation poses numerous challenges for incumbent enterprises. Incumbent enterprises are often laden with legacy infrastructure and applications that are deeply embedded in core transactional systems. Incumbent enterprises are also often stymied by institutional constraints that impede their ability to solve complex problems and rapidly respond to shifting competitive dynamics, as well as ingrained traditional approaches to development. Likewise, internal IT teams at incumbent enterprises often struggle to absorb the rapid pace of technology development and its growing complexity. To effectively harness the power of technology, incumbent enterprises need talent in ideation, strategy, user experience, Agile development and next-generation technologies. While incumbent enterprises have historically looked to traditional information technology, or IT, service providers to undertake technology development projects, these traditional players were built to serve, and remain focused on serving, legacy systems using offshore delivery.

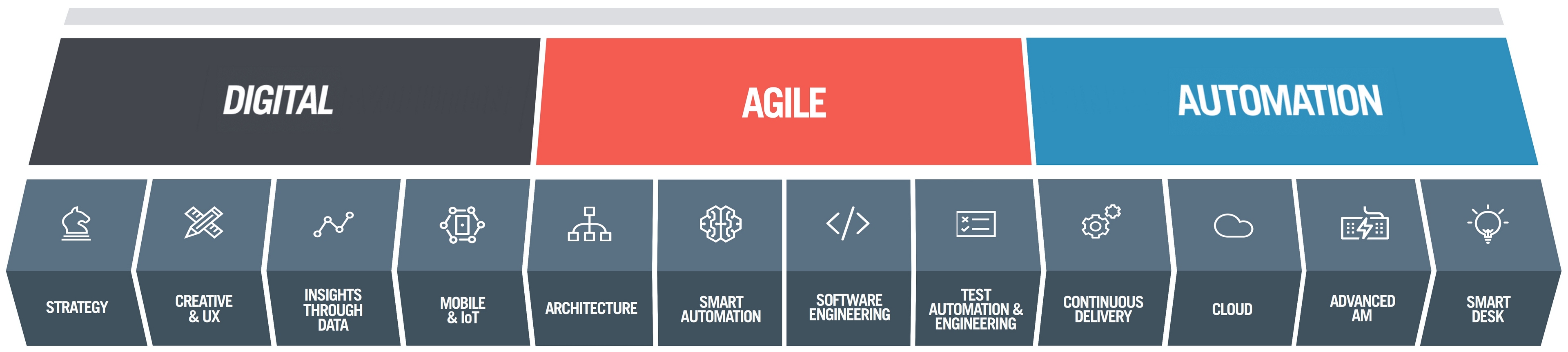

We help our clients become digital, experience-driven businesses by assisting them in their journey from idea generation to development and deployment of products, platforms and solutions. Our expertise spans the ideation-to-production spectrum across three broad solution areas – Digital Evolution, Agile Transformation and Automation. At the core of our approach is our proprietary Distributed Enterprise Agile scaling framework, known as The Endava Agile Scaling framework, or TEAS. TEAS utilizes common Agile scaling frameworks, but enhances them by balancing the requirements of delivering both quality and speed-to-market, helping our clients release higher-quality products to market faster, respond better to market changes and incorporate customer and user feedback through rapid releases and product iterations. Our deep familiarity with technologies developed over the last decade including mobile connectivity, social media, automation, big data analytics and cloud delivery, as well as next-generation technologies such as IoT, artificial intelligence, machine learning, augmented reality, virtual reality and blockchain, allows us to help our clients transform their businesses.

2

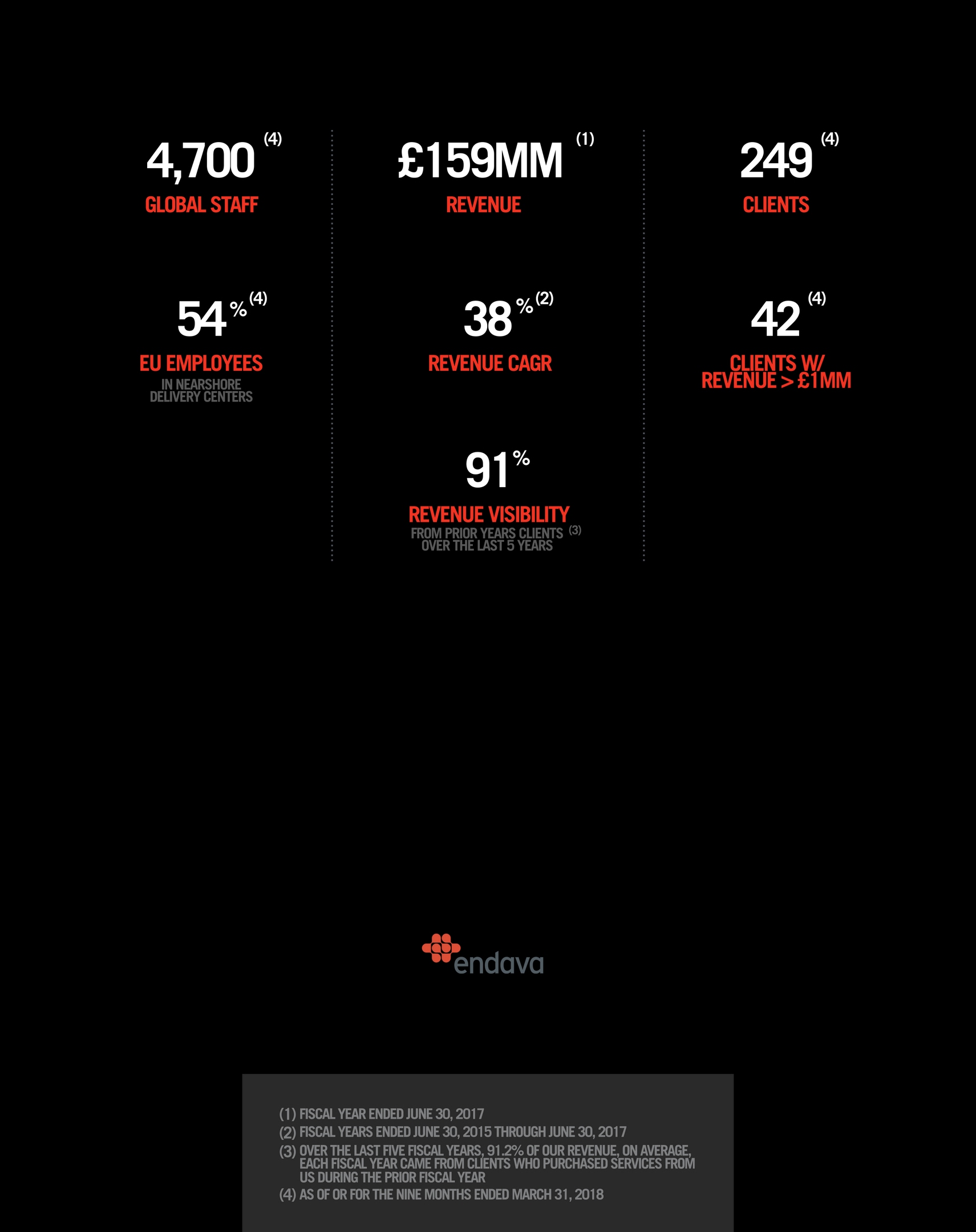

We locate our nearshore delivery centers in countries that not only have abundant IT talent pools, but also offer us an opportunity to be a preferred employer. We provide services from our nearshore delivery centers, located in two European Union countries – Romania and Bulgaria, three other Central Europe countries – Macedonia, Moldova and Serbia, and four countries in Latin America – Argentina, Colombia, Uruguay and Venezuela. We have close-to-client offices in four Western European countries – Denmark, Germany, the Netherlands and the United Kingdom, as well as in the United States. As of March 31, 2018, we had 4,700 employees, approximately 53.7% of whom work in nearshore delivery centers in European Union countries.

As of March 31, 2018, we had 249 active clients, which we define as clients who paid us for services over the preceding 12-month period. We have achieved significant growth in recent periods. For the fiscal years ended June 30, 2015, 2016 and 2017, our revenue was £84.1 million, £115.4 million and £159.4 million, respectively, representing a compound annual growth rate of 37.7% over the three year period. For the nine months ended March 31, 2017 and 2018, our revenue was £116.3 million and £156.1 million, respectively. We generated 77.8%, 64.4% and 50.2% of our revenue for the three fiscal years ended June 30, 2015, 2016 and 2017, respectively, from clients located in the United Kingdom; we generated 12.0%, 17.5% and 33.6% of our revenue in each of those fiscal years, respectively, from clients located in Europe; and we generated the balance of our revenue for each of those fiscal years from clients located in North America. Our revenue growth rate at constant currency, which is a measure that is not calculated and presented in accordance with International Financial Reporting Standards, or IFRS, for the fiscal years ended June 30, 2015, 2016 and 2017 was 32.6%, 36.6% and 28.5% respectively. Our revenue growth rate at constant currency for the nine months ended March 31, 2017 and 2018 was 28.8% and 34.6%, respectively. Over the last five fiscal years, 91.2% of our revenue, on average, each fiscal year came from clients who purchased services from us during the prior fiscal year. Our profit before taxes was £15.2 million, £20.8 million and £21.7 million for the fiscal years ended June 30, 2015, 2016 and 2017, respectively, and our profit before taxes as a percentage of revenue was 18.1%, 18.0% and 13.6%, respectively, for the same periods. Our profit before taxes was £16.2 million and £18.0 million for the nine months ended March 31, 2017 and 2018, respectively, and our profit before taxes as a percentage of revenue was 13.9% and 11.5%, respectively, for the same periods. Our adjusted profit before taxes margin, or Adjusted PBT Margin, which is a measure that is not calculated and presented in accordance with IFRS, was 19.2%, 19.7% and 15.8%, respectively, for the fiscal years ended June 30, 2015, 2016 and 2017. Our Adjusted PBT Margin was 15.8% and 15.3%, respectively, for the nine months ended March 31, 2017 and 2018. See notes 1 and 6 in the section of this prospectus titled “Summary Consolidated Financial Data – Non-IFRS Measures and Other Management Metrics” for a reconciliation of revenue growth rate at constant currency revenue growth rate and for a reconciliation of Adjusted PBT to profit before taxes, respectively, the most directly comparable financial measures calculated and presented in accordance with IFRS.

Industry Background

Overview

Significant Technology Innovation

The use of mobile connectivity, social media, automation, big data analytics and cloud delivery have become integral to business execution and emerging trends and technologies hold the potential to significantly reshape industries. Because each new generation of technology builds on and advances the technology that came before it, the pace of technological innovation will continue to accelerate, increasing the pace at which enterprises will need to transform.

Empowered Customers and Users

The proliferation of new technologies has empowered customers and users across industries and increased their expectations. Empowered customers and users are increasingly discerning and their preferences keep changing as technology evolves.

Rise of the Digital Natives

These significant technological changes have enabled the emergence of digital native companies, which leverage emerging technologies in every aspect of their businesses and are nimble and innovative, data driven and focused on the user experience. Digital native companies have revolutionized the way technology is used across all functions in

3

an organization, how technology infrastructure is built and maintained and how technology solutions are developed, deployed and continually improved.

Increasing Adoption of the Agile Approach

The adoption of Agile development, an iterative and incremental methodology premised on collaboration between cross-functional teams, has become pervasive. Agile is user driven and focused on continuous delivery of small upgrades, facilitating highly differentiated speeds of innovation and time to market.

Challenges to Transformation

There are several challenges that incumbent enterprises face in achieving technological transformation:

Significant Investment in Legacy Technology

Incumbent enterprises are often laden with legacy infrastructure and applications that are difficult and expensive to operate and maintain. For most incumbent enterprises, reorienting IT operations with new technology is expensive, time-consuming and risks service disruption.

Barriers to Innovation

Incumbent enterprises are fundamentally built to do what they are already doing and can struggle with innovation. They are often characterized by ingrained processes and cultural norms that can impede their ability to solve complex problems and rapidly respond to shifting competitive dynamics.

Not Built for Agile

Incumbent enterprises are often stymied by ingrained traditional approaches to development. The Agile methodology stands in stark contrast to the IT-department-driven, legacy approach often used by incumbent enterprises, which is premised on a sequential and siloed structure, involves long development cycles, fails to integrate user feedback and is often more costly.

Lack of Required Expertise and Talent

Internal IT teams at incumbent enterprises often struggle to absorb the rapid pace of technology development and its growing complexity. Incumbent enterprises need to acquire and retain talent in ideation, strategy, user experience, Agile development and next-generation technologies.

Limitations of Traditional IT Service Providers

Incumbent enterprises have historically looked to traditional IT service providers to undertake technology development projects. Traditional IT service providers are built for commoditized development, integration and maintenance engagements, where cost is key. While some of these traditional IT service providers have invested in capabilities to provide user experience strategy and design, as well as Agile development capabilities, they were built to serve, and remain focused on serving, legacy systems using offshore delivery.

Our Opportunity

According to International Data Corporation, or IDC, the worldwide market for digital transformation services is expected to be approximately $390 billion in 2018 and is expected to grow at a compound annual growth rate of 19.7% through 2021.

Our Competitive Strengths

We have distinguished ourselves as a leader in next-generation technology services by leveraging the following competitive strengths:

• |

Ideation through Production. We help our clients become digital, experience-driven businesses by assisting them in their journey from idea generation to development and deployment of products, platforms and solutions.

|

4

Our expertise spans the ideation-to-production spectrum across three broad solution areas – Digital Evolution, Agile Transformation and Automation.

• |

Proprietary Framework for Distributed Enterprise Agile at Scale. To allow us to deliver Distributed Enterprise Agile at scale, we have developed a proprietary Agile scaling framework, TEAS. TEAS utilizes common Agile scaling frameworks, but enhances them by balancing the requirements of delivering both quality and speed-to-market.

|

• |

Expertise in Next-Generation Technologies. We have deep expertise in next-generation technologies that drives our ability to provide solutions for Digital Evolution, Agile Transformation and Automation. Our expertise ranges from technologies developed over the last decade including mobile connectivity, social media, automation, big data analytics and cloud delivery to next-generation technologies such as IoT, artificial intelligence, machine learning, augmented reality, virtual reality and blockchain.

|

• |

Strong Domain Expertise. We have deep expertise in industry verticals that are being disrupted by technological change, particularly Payments and Financial Services and Technology, Media and Telecommunications.

|

• |

Employer of Choice in Regions with Deep Pools of Talent. We strive to be one of the leading employers of IT professionals in the regions in which we operate. We locate our nearshore delivery centers in countries that not only have abundant IT talent pools, but also offer us an opportunity to be a preferred employer. For example, a majority of our employees are located in Romania, where we have been identified as a top employer for each of the last five years.

|

• |

Distinctive Culture and Values. We believe that our people are our most important asset. We provide Endavans with training to develop their technical and soft skills, in an environment where they are continually challenged and given opportunities to grow as professionals. We believe that we have built an organization deeply committed to helping people succeed and that our culture fosters our core values of openness, thoughtfulness and adaptability.

|

• |

Founder Led, Experienced and Motivated Management Team. Our management team, led by John Cotterell, our founder and chief executive officer, has significant experience in the global technology and services industries. Our most senior 38 employees have an average tenure at Endava of 11 years.

|

Our Strategy

We are focused on continuing to distinguish ourselves as a leader in next-generation technology services. The key elements of our strategy include:

• |

Expand Relationships with Existing Clients. We are focused on continuing to expand our relationships with existing clients by helping them solve new problems and become more engaging, responsive and efficient.

|

• |

Establish New Client Relationships. We believe that we have a significant opportunity to add new clients in our existing core industry verticals and geographies, and to expand our client base to new industry verticals and geographies.

|

• |

Lead Adoption of Next-Generation Technologies. We seek to apply our creative skills and deep digital technical engineering capabilities to enhance our clients’ value to their end customers and users. As a result, we are highly focused on remaining at the forefront of emerging technology trends.

|

• |

Expand Scale in Nearshore Delivery. As we continue to expand our relationships with existing clients and attract new clients, we plan to expand our teams at existing delivery centers and open new delivery centers in nearshore locations with an abundance of technical talent.

|

• |

Selectively Pursue “Tuck-In” Acquisitions. We have a demonstrated track record of successfully identifying, acquiring and integrating complementary business and plan to leverage this experience as we pursue our “tuck-in” acquisition strategy.

|

5

Selected Risks Affecting Our Business

Investing in our ADSs involves risk. You should carefully consider all the information in this prospectus prior to investing in our ADSs. These risks are discussed more fully in the section entitled “Risk Factors” immediately following this prospectus summary. These risks and uncertainties include, but are not limited to, the following:

• |

We may not be able to sustain our revenue growth rate in the future. |

• |

We are dependent on our largest clients. |

• |

We must attract and retain highly-skilled IT professionals. |

• |

Our revenue is dependent on a limited number of industry verticals. |

• |

Our profitability could suffer if we are not able to maintain favorable pricing. |

• |

Recent acquisitions and potential future acquisitions could prove difficult to integrate, disrupt our business, dilute shareholder value and strain our resources. |

• |

We are focused on growing our client base in North America and may not be successful. |

• |

We face intense competition. |

• |

We are dependent on our senior management team and key employees. |

• |

If we are unable to comply with our security obligations or our computer systems are or become vulnerable to security breaches, we may face reputational damage and lose clients and revenue. |

• |

The United Kingdom’s withdrawal from the European Union may have a negative effect on global economic conditions, financial markets and our business. |

• |

Fluctuations in currency exchange rates and increased inflation could materially adversely affect our financial condition and results of operations. |

• |

Our international operations involve risks that could increase our expenses, adversely affect our results of operations and require increased time and attention from our management. |

• |

The three class structure of our ordinary shares has the effect of concentrating voting control for the foreseeable future, which will limit your ability to influence corporate matters. Following the completion of this offering, holders of our Class B ordinary shares will collectively beneficially hold shares representing approximately % of the voting rights of our outstanding share capital and John Cotterell, our Chief Executive Officer, will beneficially hold Class B ordinary shares representing approximately % of the voting rights of our outstanding share capital. Notwithstanding this concentration of control, we do not expect that we will qualify as a “controlled company” under New York Stock Exchange listing rules. |

Corporate Information

The legal and commercial name of our company is Endava Limited. We were registered under the laws of England and Wales in 2006 with an indefinite life.

Our principal executive office is located at 125 Old Broad Street, London EC2N 1AR, United Kingdom and our telephone number is +44 20 7367 1000. Our agent for service of process in the United States is Endava Inc. Our website address is www.endava.com. Information contained on, or that can be accessed through, our website is not incorporated by reference into this prospectus, and you should not consider information on our website to be part of this prospectus.

“Endava,” the Endava logo and other trademarks or service marks of Endava Limited appearing in this prospectus are the property of Endava or our subsidiaries. This prospectus contains additional trade names, trademarks and service marks of others, which are the property of their respective owners. Solely for convenience, trademarks and trade names referred to in this prospectus may appear without the ® or TM symbols.

6

Corporate Reorganization

Pursuant to the terms of a corporate reorganization to be effected prior to the completion of this offering, all shareholders of Endava Limited were given the choice to elect to accept redesignation of all existing ordinary shares in the capital of Endava Limited held by them into the same number of either (i) Class B ordinary shares of Endava Limited, where each Class B ordinary share is entitled to 10 votes per share and is subject to certain restrictions on transfer for a period of five years following the date of this prospectus or (ii) Class C ordinary shares of Endava Limited, where each Class C ordinary share is entitled to one vote per share and is subject to certain restrictions on transfer for a period of 18 months following the date of this prospectus, and with each Class B ordinary share and each Class C ordinary share being capable of conversion into one Class A ordinary share; provided, that the Endava Limited Guernsey Employee Benefit Trust was required to redesignate all of the existing ordinary shares held by it into the same number of Class A ordinary shares, each entitled to one vote per share. Following the corporate reorganization but prior to the completion of this offering, Endava Limited will re-register as a public limited company and change its name to Endava plc. See “Corporate Reorganization.”

Implications of Being an Emerging Growth Company

We are an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012, or the JOBS Act. As such, we may take advantage of certain exemptions from various reporting requirements that are applicable to other publicly traded entities that are not emerging growth companies. These exemptions include:

• |

the option to present only two years of audited financial statements and related discussion in the section titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in this prospectus; |

• |

not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act of 2002; and |

• |

not being required to comply with any requirement that may be adopted by the Public Company Accounting Oversight Board regarding mandatory audit firm rotation or a supplement to the auditor’s report providing additional information about the audit and the financial statements (i.e., an auditor discussion and analysis). |

As a result, we do not know if some investors will find our ADSs less attractive. The result may be a less active trading market for our ADSs, and the price of our ADSs may become more volatile.

Section 107 of the JOBS Act also provides that an emerging growth company that prepares its financial statements in accordance with U.S. GAAP can take advantage of the extended transition period provided in Section 13(a) of the Securities Exchange Act of 1934, as amended, or the Exchange Act, for complying with new or revised accounting standards. As a result, an emerging growth company can delay the adoption of certain U.S. GAAP accounting standards until those standards would otherwise apply to private companies. We will comply with new or revised accounting standards on the relevant dates on which adoption of such standards is required by the IASB.

We will remain an emerging growth company until the earliest of: (1) the last day of the first fiscal year in which our annual gross revenue exceeds $1.07 billion; (2) the last day of 2023; (3) the date that we become a “large accelerated filer” as defined in Rule 12b-2 under the Exchange Act, which would occur on the last day of any fiscal year that the aggregate worldwide market value of our common equity held by non-affiliates exceeds $700 million as of the last business day of our most recently completed second fiscal quarter; or (4) the date on which we have issued more than $1.0 billion in non-convertible debt securities during any three-year period.

Implications of Being a Foreign Private Issuer

Upon the completion of this offering, we will report under the Exchange Act as a non-U.S. company with foreign private issuer status. Even after we no longer qualify as an emerging growth company, as long as we qualify as a foreign private issuer under the Exchange Act we will be exempt from certain provisions of the Exchange Act that are applicable to U.S. domestic public companies, including:

• |

the sections of the Exchange Act regulating the solicitation of proxies, consents or authorizations in respect of a security registered under the Exchange Act; |

7

• |

the sections of the Exchange Act requiring insiders to file public reports of their stock ownership and trading activities and liability for insiders who profit from trades made in a short period of time; and |

• |

the rules under the Exchange Act requiring the filing with the SEC of quarterly reports on Form 10-Q containing unaudited financial and other specific information, and current reports on Form 8-K upon the occurrence of specified significant events. |

Foreign private issuers are also are exempt from certain more stringent executive compensation disclosure rules. Thus, even if we no longer qualify as an emerging growth company, but remain a foreign private issuer, we will continue to be exempt from the more stringent compensation disclosures required of companies that are neither an emerging growth company nor a foreign private issuer.

8

THE OFFERING

ADSs offered by us |

ADSs, each ADS representing one Class A ordinary share |

|

ADSs offered by the selling shareholders |

ADSs, each ADS representing one Class A ordinary share |

|

|

Class A ordinary shares to be outstanding after

this offering

|

shares

|

|

|

Class B ordinary shares to be outstanding after

this offering

|

5,764,525 shares |

|

Class C ordinary shares to be outstanding after this offering |

3,255,508 shares |

|

|

Total Class A ordinary shares, Class B ordinary

shares and Class C ordinary shares to be outstanding after this offering

|

shares

|

|

American Depositary Shares |

Each ADS represents one Class A ordinary share, with a nominal value of £0.10 per share. The ADSs may be evidenced by American Depositary Receipts, or ADRs. The depositary will hold the Class A ordinary shares underlying the ADSs, and you will have the rights of an ADS holder or beneficial owner (as applicable) as provided in the deposit agreement among us, the depositary and holders and beneficial owners of ADSs from time to time. To better understand the terms of our ADSs, see “Description of American Depositary Shares.” We also encourage you to read the deposit agreement, the form of which is filed as an exhibit to the registration statement of which this prospectus forms a part. |

|

Depositary |

Citibank, N.A. |

|

Over-allotment option |

Certain of the selling shareholders have granted the underwriters an option for a period of 30 days from the date of this prospectus to purchase up to an additional ADSs. |

|

9

Voting rights |

Following this offering we will have three classes of authorized ordinary shares: Class A ordinary shares, Class B ordinary shares and Class C ordinary shares. The rights of the holders of Class A ordinary shares, Class B ordinary and Class C ordinary shares are identical, except with respect to voting, conversion and transfer. The holders of Class A ordinary shares are entitled to one vote per share, the holders of Class B ordinary shares are entitled to ten votes per share and the holders of Class C ordinary shares are entitled to one vote per share on all matters that are subject to shareholder vote. Each Class B ordinary share and Class C ordinary share may be converted into one Class A ordinary share at the option of its holder, subject to certain restrictions, and will be automatically converted into one Class A ordinary share upon transfer thereof, subject to certain exceptions. In addition, (i) on the date that the outstanding Class B ordinary shares represent less than 10% of the aggregate voting power of our share capital, all outstanding Class B ordinary shares will convert automatically into Class A ordinary shares and (ii) on the date that is two years from the date of this prospectus, all Class C ordinary shares will convert automatically into Class A ordinary shares. See “Description of Share Capital and Articles of Association.” |

|

Restriction on transfer |

We, our executive officers, directors and holders of substantially all of our outstanding ordinary shares (including all of the selling shareholders) have agreed that, subject to certain exceptions, for a period of 180 days from the date of this prospectus, we and they will not, without the prior written consent of Morgan Stanley & Co. LLC, dispose of or hedge any ADSs or shares or any securities convertible into or exchangeable for shares of our company. Morgan Stanley & Co. LLC may, at its discretion, release or waive any of the securities subject to these lock-up agreements at any time. |

|

In addition, our articles of association provide that (i) each holder of Class B ordinary shares may not dispose of (a) any Class B ordinary shares during the period ending 180 days from the date of this prospectus, (b) more than 25% of the Class B ordinary shares held by such holder as of the date of this prospectus in the 18-month period following the date of this prospectus (including by conversion to Class A ordinary shares), (c) more than 40% of the Class B ordinary shares held by such holder as of the date of this prospectus in the three-year period following the date of this prospectus (including by conversion to Class A ordinary shares) and (d) more than 60% of the Class B ordinary shares held by such holder as of the date of this prospectus in the five-year period following the date of this prospectus (including by conversion to Class A ordinary shares) and (ii) each holder of Class C ordinary shares may not dispose of (a) any Class C ordinary shares during the period ending 180 days from the date of this prospectus or (b) more than 25% of the Class C ordinary shares held by such holder as of the date of this prospectus in the 18-month period following the date of this prospectus (including by conversion to Class A ordinary shares). |

||

10

All of our directors and officers and certain of our other employees have agreed to receive Class B ordinary shares in exchange for all ordinary shares currently held by them. See “Description of Share Capital and Articles of Association.” |

||

Use of proceeds |

We estimate that the net proceeds from our sale of ADSs in this offering will be approximately $ million (£ million), assuming an initial public offering price of $ per ADS, the midpoint of the price range set forth on the cover page of this prospectus, and after deducting the estimated underwriting discounts and commissions and estimated offering expenses payable by us.

The principal purposes of this offering are to increase our capitalization and financial flexibility and create a public market for our ADSs. We intend to use the net proceeds we receive from this offering to repay in full amounts outstanding under our revolving credit facility with HSBC Bank PLC and for general corporate purposes, including working capital, selling, general and administrative expenses and capital expenditures.

See “Use of Proceeds” for additional information.

We will not receive any of the proceeds from the sale of ADSs by the selling shareholders.

|

|

Risk factors |

See “Risk Factors” and the other information included in this prospectus for a discussion of factors you should carefully consider before deciding to invest in our ADSs. |

|

Proposed New York Stock Exchange symbol |

“DAVA” |

|

The number of our Class A ordinary shares, Class B ordinary shares and Class C ordinary shares that will be outstanding after this offering is based on 9,960,829 ordinary shares outstanding as of March 31, 2018, and excludes:

• |

33,846 Class A ordinary shares issuable upon the exercise of share options outstanding as of March 31, 2018, at a weighted average exercise price of £4.33 per share, with the balance of the total number of 974,642 Class A ordinary shares subject to share options outstanding as of March 31, 2018 being currently issued and outstanding and held by the Endava Limited Guernsey Employee Benefit Trust; |

• |

Class A ordinary shares that will be issued, following the completion of this offering, in connection with our acquisition of Velocity Partners LLC, or Velocity Partners, assuming a public offering price of $ per ADS, the midpoint of the price range set forth on the cover of this prospectus;

|

• |

Class A ordinary shares reserved for future issuance pursuant to our 2018 Equity Incentive Plan, which will become effective prior to the completion of this offering and includes provisions that automatically increase the number of Class A ordinary shares reserved for issuance thereunder each year, and which number of reserved shares includes Class A ordinary shares that we will be required to issue to certain continuing employees of Velocity Partners over a period of three years following the completion of this offering; and |

• |

Class A ordinary shares reserved for future issuance pursuant to the Endava plc 2018 Sharesave Plan, which will become effective prior to the completion of this offering and includes provisions that automatically increase the number of Class A ordinary shares reserved for issuance thereunder each year. |

11

Unless otherwise indicated, this prospectus reflects and assumes the following:

• |

the redesignation of an aggregate of 940,796 of our outstanding ordinary shares into an aggregate of 940,796 Class A ordinary shares prior to the completion of this offering; |

• |

the redesignation of an aggregate of 5,764,525 of our outstanding ordinary shares into an aggregate of 5,764,525 Class B ordinary shares prior to the completion of this offering; |

• |

the redesignation of an aggregate of 3,255,508 of our outstanding ordinary shares into an aggregate of 3,255,508 Class C ordinary shares prior to the completion of this offering; |

• |

the modification of all outstanding options to acquire ordinary shares into options to acquire an equal number of redesignated Class A ordinary shares prior to the completion of this offering; |

• |

the completion of the transactions described in the section of this prospectus titled “Corporate Reorganization”; |

• |

a -for-one share split of each class of our ordinary shares effected on , 2018; |

• |

no exercise of outstanding share options after March 31, 2018; and |

• |

no exercise of the underwriters’ over-allotment option. |

12

SUMMARY CONSOLIDATED FINANCIAL DATA

The following tables set forth our summary consolidated financial data for the periods indicated. We have derived the consolidated statement of comprehensive income for the fiscal years ended June 30, 2016 and 2017 and the consolidated balance sheet data as of June 30, 2017 from our audited consolidated financial statements included elsewhere in this prospectus. In order to provide additional historical financial information, we have included supplemental unaudited consolidated statements of operation data for the fiscal year ended June 30, 2015, which is derived from the consolidated statement of comprehensive income for the fiscal year ended June 30, 2015 from our unaudited financial statements not included elsewhere in this prospectus. We derived the consolidated statement of comprehensive income for the nine months ended March 31, 2017 and 2018 and the consolidated balance sheet as of March 31, 2018 from our unaudited condensed consolidated financial statements included elsewhere in this prospectus. We have prepared the unaudited consolidated financial statements on the same basis as the audited consolidated financial statements. In the opinion of management, the unaudited financial statements reflect all adjustments, consisting only of normal, recurring adjustments, necessary for a fair statement of the financial information in those statements. Our historical results are not necessarily indicative of the results that should be expected for any future period, and our results for the nine months ended March 31, 2018 are not necessarily indicative of the results to be expected for the full fiscal year. You should read the following summary consolidated financial data together with the audited consolidated financial statements included elsewhere in this prospectus and the sections titled “Exchange Rate Information” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

We maintain our books and records in British Pounds, and we prepare our financial statements in accordance with IFRS as issued by the IASB. We report our financial results in British Pounds.

13

Fiscal Year Ended June 30, |

Nine Months Ended March 31, |

||||||||||||||||||||||||||

2015 (£) |

2016 (£) |

2017 (£) |

2017 ($)(1)

|

2017 (£) |

2018 (£) |

2018 ($)(1)

|

|||||||||||||||||||||

(in thousands, except for share and per share amounts) |

|||||||||||||||||||||||||||

Consolidated Statements of Operations Data: |

|||||||||||||||||||||||||||

Revenue |

£ |

84,107 |

£ |

115,432 |

£ |

159,368 |

$ |

223,625 |

£ |

116,322 |

£ |

156,140 |

$ |

219,096 |

|||||||||||||

Cost of sales: |

|||||||||||||||||||||||||||

Direct cost of sales(2)

|

(49,717 |

) |

(68,517 |

) |

(98,853 |

) |

(138,711 |

) |

(72,692 |

) |

(96,104 |

) |

(134,853 |

) |

|||||||||||||

Allocated cost of sales |

(3,674 |

) |

(6,529 |

) |

(9,907 |

) |

(13,902 |

) |

(6,943 |

) |

(9,281 |

) |

(13,023 |

) |

|||||||||||||

Total cost of sales |

(53,391 |

) |

(75,046 |

) |

(108,760 |

) |

(152,613 |

) |

(79,635 |

) |

(105,385 |

) |

(147,876 |

) |

|||||||||||||

Gross profit |

30,716 |

40,386 |

50,608 |

71,012 |

36,687 |

50,755 |

71,220 |

||||||||||||||||||||

Selling, general and administrative expenses(2)

|

(13,729 |

) |

(20,453 |

) |

(27,551 |

) |

(38,660 |

) |

(19,993 |

) |

(31,755 |

) |

(44,559 |

) |

|||||||||||||

Operating profit |

16,987 |

19,933 |

23,057 |

32,352 |

16,694 |

19,000 |

26,661 |

||||||||||||||||||||

Net finance (costs)/income |

(1,781 |

) |

898 |

(1,357 |

) |

(1,904 |

) |

(515 |

) |

(1,030 |

) |

(1,445 |

) |

||||||||||||||

Profit before tax |

15,206 |

20,831 |

21,700 |

30,448 |

16,179 |

17,970 |

25,216 |

||||||||||||||||||||

Tax on profit on ordinary activities |

(1,659 |

) |

(4,125 |

) |

(4,868 |

) |

(6,831 |

) |

(3,629 |

) |

(3,893 |

) |

(5,463 |

) |

|||||||||||||

Net profit |

£ |

13,547 |

£ |

16,706 |

£ |

16,832 |

$ |

23,617 |

£ |

12,550 |

£ |

14,077 |

$ |

19,753 |

|||||||||||||

Earnings per share, basic |

£ |

1.76 |

£ |

1.84 |

£ |

1.86 |

$ |

2.61 |

£ |

1.39 |

£ |

1.56 |

$ |

2.19 |

|||||||||||||

Earnings per share, diluted |

£ |

1.47 |

£ |

1.69 |

£ |

1.71 |

$ |

2.40 |

£ |

1.27 |

£ |

1.42 |

$ |

1.99 |

|||||||||||||

Weighted average number of shares outstanding, basic |

7,696,492 |

9,077,842 |

9,051,750 |

9,051,750 |

9,060,100 |

9,020,033 |

9,020,033 |

||||||||||||||||||||

Weighted average number of shares outstanding, diluted |

9,230,051 |

9,863,609 |

9,858,504 |

9,858,504 |

9,874,961 |

9,911,426 |

9,911,426 |

||||||||||||||||||||

Other Financial Data: |

|||||||||||||||||||||||||||

Revenue period-over-period growth rate |

31.6 |

% |

37.2 |

% |

38.1 |

% |

39.4 |

% |

34.2 |

% |

|||||||||||||||||

Profit before tax margin |

18.1% |

18.0% |

13.6% |

13.9% |

11.5% |

||||||||||||||||||||||

Net cash provided by (used in) operating activities |

£11,107 |

£10,897 |

£14,740 |

£3,788 |

£20,374 |

||||||||||||||||||||||

(1) |

Translated solely for convenience into dollars at the rate of £1.00 = $1.4032. |

(2) |

Includes share-based compensation expenses as follows: |

Fiscal Year Ended June 30, |

Nine Months Ended March 31, |

||||||||||||||||||

2015 |

2016 |

2017 |

2017 |

2018 |

|||||||||||||||

(in thousands) |

|||||||||||||||||||

Direct cost of sales |

£ |

115 |

£ |

587 |

£ |

560 |

£ |

448 |

£ |

686 |

|||||||||

Selling, general and administrative expenses |

65 |

181 |

294 |

228 |

340 |

||||||||||||||

Total |

£ |

180 |

£ |

768 |

£ |

854 |

£ |

676 |

£ |

1,026 |

|||||||||

14

As of March 31, 2018 |

|||||

Actual |

As Adjusted(1)(2)

|

||||

Consolidated Balance Sheet Data: |

|||||

Cash and cash equivalents |

£ |

9,462 |

£ |

||

Working capital (3)

|

(5,197 |

) |

|||

Total assets |

138,303 |

||||

Total liabilities |

75,808 |

||||

Total shareholders’ equity |

62,495 |

||||

________________

(1) |

As adjusted consolidated balance sheet data reflects the sale of ADSs in this offering at an assumed initial public offering price of $ per ADS, the midpoint of the price range set forth on the cover of this prospectus, after deducting the estimated underwriting discounts and commissions and estimated offering expenses payable by us. |

(2) |

As adjusted consolidated balance sheet data is illustrative only and will change based on the actual initial public offering price and other terms of this offering determined at pricing. Each $1.00 increase or decrease in the assumed initial public offering price of $ per ADS, the midpoint of the price range set forth on the cover of this prospectus, would increase or decrease each of as adjusted cash and cash equivalents, working capital, total assets and total shareholders’ equity by approximately £ ($ ) million, assuming that the number of ADSs offered by us, as set forth on the cover of this prospectus, remains the same, and after deducting estimated underwriting discounts and commissions and estimated offering expenses payable by us. We may also increase or decrease the number of ADS we are offering. Each 1,000,000 share increase or decrease in the number of ADSs offered by us would increase or decrease each of as adjusted cash and cash equivalents, working capital, total assets and total shareholders’ equity by approximately £ ($ ) million. |

(3) |

Working capital is defined as total current assets minus total current liabilities. |

Non-IFRS Measures and Other Management Metrics

We regularly monitor a number of financial and operating metrics to evaluate our business, measure our performance, identify trends affecting our business, formulate financial projections and make strategic decisions. Our management metrics may be calculated in a different manner than similarly titled metrics used by other companies.

Fiscal Year Ended June 30, |

Nine Months Ended March 31, |

||||||||||||||||||

2015 |

2016 |

2017 |

2017 |

2018 |

|||||||||||||||

(pounds in thousands) |

|||||||||||||||||||

Revenue growth rate at constant currency(1)

|

32.6 |

% |

36.6 |

% |

28.5 |

% |

28.8 |

% |

34.6 |

% |

|||||||||

Average number of employees involved in delivery of our services(2)

|

1,645 |

2,336 |

3,181 |

3,115 |

3,829 |

||||||||||||||

Revenue concentration(3)

|

65.5 |

% |

53.7 |

% |

49.1 |

% |

50.4 |

% |

43.1 |

% |

|||||||||

Number of large clients(4)

|

18 |

26 |

34 |

36 |

42 |

||||||||||||||

Adjusted profit before taxes margin(5)

|

19.2 |

% |

19.7 |

% |

15.8 |

% |

15.8 |

% |

15.3 |

% |

|||||||||

Free cash flow(6)

|

£ |

9,492 |

£ |

10,115 |

£ |

11,186 |

£ |

370 |

£ |

17,500 |

|||||||||

(1) |

We monitor our revenue growth rate at constant currency. As the impact of foreign currency exchange rates is highly variable and difficult to predict, we believe revenue growth rate at constant currency allows us to better understand the underlying business trends and performance of our ongoing operations on a period-over-period basis. We calculate revenue growth rate at constant currency by translating revenue from entities reporting in foreign currencies into British Pounds using the comparable foreign currency exchange rates from the prior period. For example, the average rates in effect for the fiscal year ended June 30, 2016 were used to convert revenue for the fiscal year ended June 30, 2017 and the revenue for the comparable prior period ended June 30, 2016, rather than the actual exchange rates in effect during the respective period. Revenue growth rate at constant currency is not a measure calculated in accordance with IFRS. While we believe that revenue growth rate at constant currency provides useful information to investors in understanding and evaluating our results of operations in the same manner as our management, our use of revenue growth rate at constant currency has limitations as an analytical tool, and you should not consider it in isolation or as a substitute for analysis of our financial results as reported under IFRS. Further, other companies, including companies in our industry, may report the impact of fluctuations in foreign currency exchange rates differently, which |

15

may reduce the value of our revenue growth rate at constant currency as a comparative measure. The following table presents a reconciliation of revenue growth rate at constant currency to revenue growth rate, the most directly comparable financial measure calculated and presented in accordance with IFRS, for each of the periods indicated:

Fiscal Year Ended June 30, |

Nine Months Ended March 31, |

||||||||||||||||||

2015 |

2016 |

2017 |

2017 |

2018 |

|||||||||||||||

(pounds in thousands) |

|||||||||||||||||||

Revenue |

£ |

84,107 |

£ |

115,432 |

£ |

159,368 |

£ |

116,322 |

£ |

156,140 |

|||||||||

Revenue period-over-period growth rate |

31.6 |

% |

37.2 |

% |

38.1 |

% |

39.4 |

% |

34.2 |

% |

|||||||||

Estimated impact of foreign currency exchange rate fluctuations |

1.0 |

% |

(0.6 |

)% |

(9.6 |

)% |

(10.6 |

)% |

0.4 |

% |

|||||||||

Revenue growth rate at constant currency |

32.6 |

% |

36.6 |

% |

28.5 |

% |

28.8 |

% |

34.6 |

% |

|||||||||

(2) |

We monitor our average number of employees involved in delivery of our services because we believe it gives us visibility to the size of both our revenue-producing base and our most significant cost base, which in turn allows us better understand changes in our utilization rates and gross margins on a period-over-period basis. We calculate average number of employees involved in delivery of our services as the average of our number of full-time employees involved in delivery of our services on the last day of each month in the relevant period. |

(3) |

We monitor our revenue concentration to better understand our dependence on large clients on a period-over-period basis and to monitor our success in diversifying our revenue basis. We define revenue concentration as the percent of our total revenue derived from our 10 largest clients by revenue in each period presented. |

(4) |

We monitor our number of large clients to better understand our progress in winning large contracts on a period-over-period basis. We define number of large clients as the number of clients from whom we generated more than £1.0 million of revenue in the prior 12-month period. |

(5) |

We monitor our adjusted profit before taxes margin, or Adjusted PBT Margin, to better understand our ability to manage operational costs, to evaluate our core operating performance and trends and to develop future operating plans. In particular, we believe that the exclusion of certain expenses in calculating Adjusted PBT Margin facilitates comparisons of our operating performance on a period-over-period basis. Our Adjusted PBT Margin is our Adjusted PBT, which is our profit before taxes adjusted to exclude the impact of share-based compensation expense, amortization of acquired intangible assets, realized and unrealized foreign currency exchange gains and losses and initial public offering expenses incurred (all of which are non-cash other than realized foreign currency exchange gains and losses and initial public offering expenses), as a percentage of our total revenue. We do not consider these excluded items to be indicative of our core operating performance. Adjusted PBT Margin is not a measure calculated in accordance with IFRS. While we believe that Adjusted PBT Margin provides useful information to investors in understanding and evaluating our results of operations in the same manner as our management, our use of Adjusted PBT Margin has limitations as an analytical tool, and you should not consider it in isolation or as a substitute for analysis of our financial results as reported under IFRS. For example, Adjusted PBT Margin does not reflect the potentially dilutive impact of share-based compensation nor does it reflect the potentially significant impact of foreign currency exchange rate fluctuations on our working capital. Further, other companies, including companies in our industry, may adjust their profit differently to capture their operating performance, which may reduce the value of Adjusted PBT Margin as a comparative measure. The following table presents a reconciliation of Adjusted PBT to profit before taxes, the most directly comparable financial measure calculated and presented in accordance with IFRS, for each of the periods indicated: |

Fiscal Year Ended June 30, |

Nine Months Ended March 31, |

||||||||||||||||||

2015 |

2016 |

2017 |

2017 |

2018 |

|||||||||||||||

(in thousands) |

|||||||||||||||||||

Profit before taxes |

£ |

15,206 |

£ |

20,831 |

£ |

21,700 |

£ |

16,179 |

£ |

17,970 |

|||||||||

Share-based compensation expense |

180 |

768 |

854 |

676 |

1,026 |

||||||||||||||

Amortization of acquired intangible assets |

— |

1,165 |

1,715 |

1,256 |

1,804 |

||||||||||||||

Foreign currency exchange (gains) losses, net |

754 |

(4 |

) |

967 |

213 |

545 |

|||||||||||||

Initial public offering expenses incurred |

— |

— |

— |

— |

2,472 |

||||||||||||||

Adjusted PBT |

£ |

16,140 |

£ |

22,760 |

£ |

25,236 |

£ |

18,324 |

£ |

23,817 |

|||||||||

(6) |

We monitor our free cash flow to better understand and evaluate our liquidity position and to develop future operating plans. Our free cash flow is our net cash provided by (used in) operating activities, plus grant received, less purchases of non-current tangible and intangible assets and plus initial public offering expenses paid. For a discussion of grant received, see |

16

“Management’s Discussion and Analysis of Financial Condition and Results of Operations—Components of Results of Operations—Cost of Sales.” Free cash flow is not a measure calculated in accordance with IFRS. While we believe that free cash flow provides useful information to investors in understanding and evaluating our liquidity position in the same manner as our management, our use of free cash flow has limitations as an analytical tool, and you should not consider it in isolation or as a substitute for analysis of our financial results as reported under IFRS. Further, other companies, including companies in our industry, may adjust their cash flows differently to capture their liquidity, which may reduce the value of free cash flow as a comparative measure. The following table presents a reconciliation of free cash flow to net cash provided by (used in) operating activities, the most directly comparable financial measure calculated and presented in accordance with IFRS, for each of the periods indicated:

Fiscal Year Ended June 30, |

Nine Months Ended March 31, |

||||||||||||||||||

2015 |

2016 |

2017 |

2017 |

2018 |

|||||||||||||||

(in thousands) |

|||||||||||||||||||

Net cash provided by (used in) operating activities |

£ |

11,107 |

£ |

10,897 |

£ |

14,740 |

£ |

3,788 |

£ |

20,374 |

|||||||||

Grant received |

468 |

1,948 |

2,924 |

— |

147 |

||||||||||||||

Purchases of non-current assets (tangible and intangible) |

(2,083 |

) |

(2,730 |

) |

(6,478 |

) |

(3,418 |

) |

(3,678 |

) |

|||||||||

Initial public offering expenses paid |

— |

— |

— |

— |

657 |

||||||||||||||

Free cash flow |

£ |

9,492 |

£ |

10,115 |

£ |

11,186 |

£ |

370 |

£ |

17,500 |

|||||||||

17

RISK FACTORS

Investing in our ADSs involves a high degree of risk. You should consider carefully the risks and uncertainties described below, together with all of the other information in this prospectus, including our consolidated financial statements and related notes, before deciding whether to purchase our ADSs. If any of the following risks are realized, our business, financial condition, results of operations and prospects could be materially and adversely affected. In that event, the price of our ADSs could decline, and you could lose part or all of your investment.

Risks Related to Our Business and Industry

We may not be able to sustain our revenue growth rate in the future.

We have experienced rapid revenue growth in recent periods. Our revenue increased by 38.1% from £115.4 million in the fiscal year ended June 30, 2016 to £159.4 million in the fiscal year ended June 30, 2017. We may not be able to sustain revenue growth consistent with our recent history or at all. You should not consider our revenue growth in recent periods as indicative of our future performance. As we grow our business, we expect our revenue growth rates to slow in future periods due to a number of factors, which may include slowing demand for our services, increasing competition, decreasing growth of our overall market, our inability to engage and retain a sufficient number of IT professionals or otherwise scale our business, prevailing wages in the markets in which we operate or our failure, for any reason, to capitalize on growth opportunities.

We are dependent on our largest clients.

Historically, a significant percentage of our revenue has come from our existing client base. For example, during the fiscal year ended June 30, 2017, 90.5% of our revenue came from clients from whom we generated revenue during the prior fiscal year. However, the volume of work performed for a specific client is likely to vary from year to year, especially since we generally do not have long-term commitments from our clients’ and are often not our clients’ exclusive technology services provider. A major client in one year may not provide the same level of revenue for us in any subsequent year. Further, one or more of our significant clients could get acquired and there can be no assurance that the acquirer would choose to use our services in respect of such client to the same degree as previously, if at all. In particular, some of our clients are owned by private equity firms and are therefore inherently more likely to be sold at some point in the future.

In addition, the services we provide to our clients, and the revenue and income from those services, may decline or vary as the type and quantity of services we provide changes over time. In addition, our reliance on any individual client for a significant portion of our revenue may give that client a certain degree of pricing leverage against us when negotiating contracts and terms of service. In order to successfully perform and market our services, we must establish and maintain multi-year close relationships with our clients and develop a thorough understanding of their businesses. Our ability to maintain these close relationships is essential to the growth and profitability of our business. If we fail to maintain these relationships and successfully obtain new engagements from our existing clients, we may not achieve our revenue growth and other financial goals.

During the fiscal years ended June 30, 2016 and June 30, 2017 and the nine months ended March 31, 2017 and 2018, our ten largest clients accounted for 53.7%, 49.1%, 50.4% and 43.1% of our revenue, respectively. Our largest client for the fiscal years ended June 30, 2016 and June 30, 2017 and the nine months ended March 31, 2017 and 2018, Worldpay (UK) Limited, or Worldpay, accounted for 15.6%, 13.0%, 13.2% and 11.4% of our revenue, respectively. We are party to two principal agreements with Worldpay: a master services agreement and a build and operate agreement. Under the master services agreement, Worldpay committed to spend an aggregate of £55.7 million, after giving effect to certain discounts, with us during the period from January 1, 2017 to December 31, 2021, with annual discounted commitments ranging from £9.7 million to £12.2 million. Either we or Worldpay may terminate the master services agreement for cause (including material breach by the other party) and Worldpay may terminate the master services agreement if we undergo a change of control or due to regulatory requirements. In addition, following July 1, 2018, Worldpay may terminate the master services agreement for convenience subject to six months prior notice and payment of 30% of the minimum undiscounted commitment amount for the 12-month period following termination.

18

Under the build and operate agreement, we created and staffed a captive Romanian subsidiary for Worldpay. Worldpay issues us orders to hire personnel to the captive Romanian subsidiary and we bill Worldpay for the cost of such personnel throughout the term of the build and operate agreement. Pursuant to an option and transfer agreement, Worldpay has an option to acquire the captive Romanian subsidiary from us, which may be exercised in either September 2019 or January 2020 by Worldpay giving us three months’ notice and paying us fair market value for the shares of the captive Romanian subsidiary; provided, that the aggregate purchase price will not be less than £2.5 million nor more than £6.0 million. To the extent both parties deem commercially beneficial, Worldpay may also exercise the option prior to September 2019. If Worldpay exercises its option under the option and transfer agreement, the build and operate agreement would terminate upon consummation of the option exercise. If Worldpay does not exercise its option under the option and transfer agreement, the build and operate agreement would terminate on July 31, 2020, subject to earlier termination as set forth below, following which we would be solely responsible for all costs associated with the captive Romanian subsidiary. Either we or Worldpay may terminate the build and operate agreement for cause (including material breach) and Worldpay may terminate the build and operate agreement if we undergo a change of control to a Worldpay competitor. If we terminate the build and operate agreement as a result of Worldpay’s material breach, Worldpay is required to pay us €2.0 million. In addition, Worldpay may terminate the build and operate agreement for convenience subject to six months prior notice and, if such termination occurs in 2018 or 2019, payment of between €2.0 million and €650,000. As of March 31, 2018, the captive Romanian subsidiary employed approximately 100 people, representing approximately one quarter of our total number of employees working on various projects for Worldpay as of March 31, 2018. The captive Romanian subsidiary contributed approximately 1.5% of our total revenue in the fiscal year ended June 30, 2017. If Worldpay were to exercise its option to acquire the captive Romanian subsidiary, we would immediately lose future revenue and associated cost from this captive subsidiary. In addition, the exercise of this option may increase the likelihood that Worldpay would cease engaging us for new projects, which could affect our revenue, business, results of operations and financial condition and the market price of our ADSs. In January 2018, Worldpay was acquired by Vantiv. There can be no assurance that our relationship will not be adversely affected as a result of this acquisition.

We generally do not have long-term commitments from our clients, and our clients may terminate engagements before completion or choose not to enter into new engagements with us.

Our clients are generally not obligated for any long-term commitments to us. Our clients can terminate many of our master services agreements and work orders with or without cause, in some cases subject only to 15 days’ prior notice in the case of termination without cause. Although a substantial majority of our revenue is typically generated from clients who also contributed to our revenue during the prior year, our engagements with our clients are typically for projects that are singular in nature. In addition, large and complex projects may involve multiple engagements or stages, and a client may choose not to retain us for additional stages or may cancel or delay additional planned engagements. Therefore, we must seek to obtain new engagements when our current engagements are successfully completed or are terminated as well as maintain relationships with existing clients and secure new clients to maintain and expand our business.

Even if we successfully deliver on contracted services and maintain close relationships with our clients, a number of factors outside of our control could cause the loss of or reduction in business or revenue from our existing clients. These factors include, among other things:

• |